Chartbook #12

August 1, 2021

Hello everyone and welcome back! This Chartbook will review three key events of the last week and propose some theories for how they fit together and may shape the future of money markets. In chronological order, these events were:

On the morning of July 28, the Group of Thirty (G30), an influential discussion group of international financiers, published a report (link) recommending 10 significant changes to the structure of the US Treasury and repo markets.

Later on July 28, the New York Fed announced (link) the creation of a permanent repo facility to replace temporary repo operations it had made available since September of 2019, as well as made permanent the temporary foreign official repo facility it had launched in March 2020.

On July 29 the Alternative Reference Rates Committee, a group convened by the New York Fed, formally recommended (link) Term SOFR rates as the new benchmark for interdealer swaps trading.

Let’s start by reviewing the G30 report, which focused heavily on the need for better reporting, central clearing, and stabilizing policy tools in the Treasury market. The first recommendation, quoted below, was partly implemented by the Fed on the very same day.

Recommendation 1: The Federal Reserve should create a Standing Repo Facility (SRF) that provides very broad access to repo financing for U.S. Treasury securities on terms that discourage use of the facility in normal market conditions without stigmatizing its use under stress. It should make permanent its Foreign and International Monetary Authority repo facility.

Though the Fed did create a Standing Repo Facility (SRF) last week, it does not yet provide “very broad access” as for now it is only accessible to the primary dealers, with access for depository institutions planned for later this year. The G30 report, however, recommended expanding the SRF even further by clearing its repo operations through a central counterparty, the Fixed Income Clearing Corporation (FICC):

A pragmatic and operationally efficient means by which the Fed could reach a broad range of counterparties would be by clearing its repos through the Fixed Income Clearing Corporation (FICC), which would provide access to many broker-dealers as well as banks. FICC would need to exempt the Federal Reserve from requirements for FICC members to participate in the mutualization of losses from defaults by FICC members.

This would be a notable shift from how the Fed carries out its repo operations currently, which is through tri-party repos cleared on the books of Bank of New York Mellon (see question #10 in this FAQ). While dealers do source funds from non-dealers in the non-centrally cleared tri-party repo market, moving the SRF to central clearing and broadening access to all FICC member dealers could help the Fed more seamlessly integrate its operations with the interdealer repo market, which is mostly centrally cleared. If the details of this recommendation were to be implemented, the Fed could use an existing FICC mechanism to centrally clear its tri-party trades as a non-dealer cash lender: the Centrally Cleared Institutional Tri-Party (CCIT) service (link, see pages 5-15 for a description). Like many transactions cleared through FICC, repos traded through the CCIT service are backed by a FICC guarantee of settlement. This is partly dependent on the “mutualization of losses from defaults by FICC members” as mentioned in the quote. Through a mechanism called the Capped Contingency Liquidity Facility (CCLF) (link, see pages 3-21 for description), FICC can draw on credit from non-defaulting members to meet obligations while the defaulting party’s positions are unwound in an orderly liquidation. While the CCLF benefits dealers and cash lenders who clear their trades through FICC by reducing the chances of a disorderly fire sale, it would likely not be acceptable for the Fed to be exposed to a shared counterparty risk in case of a FICC member defaulting. The G30 report thus suggests that the Fed should be exempt from contributing to the CCLF while being allowed to centrally clear its trades through FICC. Also notably, the report encourages all Treasury repos be centrally cleared:

Recommendation 3: Treasury repos should be centrally cleared.

If implemented alongside the prior recommendations, this could unlock balance sheet efficiencies for dealers and other repo market participants through the netting of trades that are not currently centrally cleared, as well as help the SRF transmit policy as effectively as possible to the broader repo market. But what does the SRF itself mean in terms of policy? Let’s move on to that announcement and put the new facility in context!

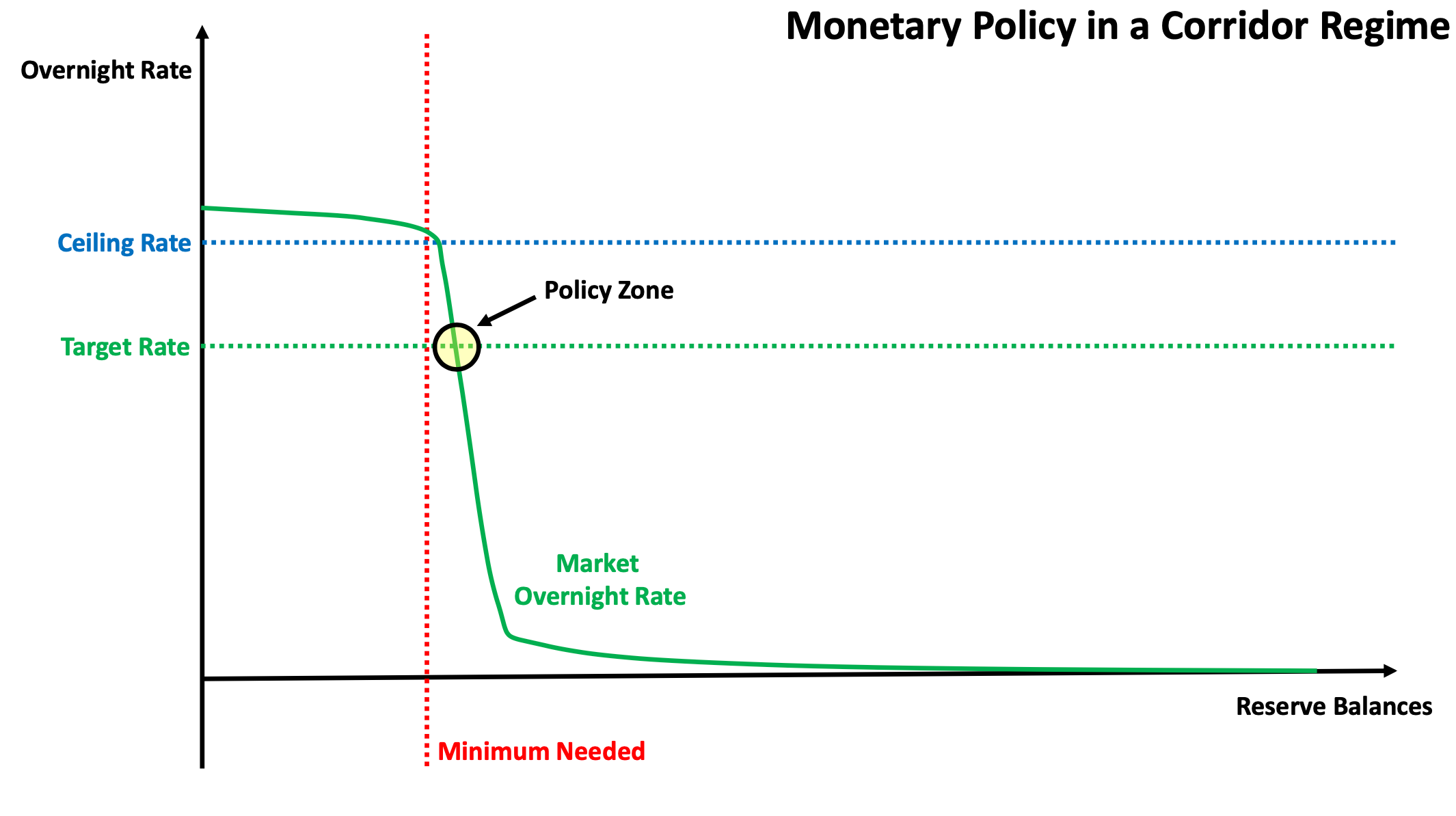

To start, let’s go back to the mid-2000s, when Fed policy was implemented in a very different way than it is today.

Prior to the 2008 financial crisis, the Fed implemented monetary policy in a corridor system, a stylized depiction of which is shown in the chart above. The x-axis of the chart shows the level of reserves in a hypothetical banking system, with the red dashed line being the minimum needed to meet regulatory and operational needs. The solid green line then shows market overnight rates as a function of the reserve level. Since reserves in the pre-2008 corridor system did not earn interest, a significant excess of reserves over needed minimums would cause market rates to quickly fall towards zero, since there would otherwise be a large opportunity cost to holding excess reserves. This is the elastic region of the overnight rates market, where the supply of cash comfortably meets demand and a marginal increase in cash levels does not affect the level of overnight rates significantly. As the level of reserves approaches the minimum, rates enter an inelastic region, where market participants are willing to pay a higher price to secure the cash needed for operations. A central bank in this system would set a ceiling for rates in the inelastic region by allowing banks to borrow from a fixed-rate facility (in the case of the pre-2008 Fed, the discount window). While banks may be reluctant to borrow from the central bank at penalty rates for reasons of public image, the existence of a fixed rate facility would prevent market rates from going too far above the ceiling in a cash shortage situation. In normal times, the central bank would target market rates somewhat lower than the ceiling by supplying or draining reserves in open market operations.

This chart shows how the Fed implemented a policy regime like this in practice in the pre-2008 era. The top panel shows the market Federal Funds rate (white line) and the ceiling (red) and target (blue) rates. The bottom panel shows the level of reserves held with Federal Reserve Banks at the time, which would fluctuate daily to maintain rates near the policy target. Since banks in this era held much lower levels of liquid assets than they are now required to, reserve levels were also much lower than they are today. This changed in October 2008, when in response to the financial crisis the Fed greatly increased the level of reserves in the banking system in an effort to stabilize money markets and started paying interest on these reserve balances (link to announcement).

The October 2008 move shifted monetary policy in the US from a corridor regime to a floor regime, which is described in this chart. While the quantity of needed reserves expanded greatly in the aftermath of the financial crisis due to increased regulation of banks, the reserves supplied by the Fed through quantitative easing kept money markets in the elastic range. By paying interest on reserves, the Fed was able to adapt its policy tools to this new regime, preventing money market rates from falling too far below the floor despite the significant excess of reserves in the system.

Currently, the Fed operates in a double floor system, where the rate of interest on reserves (yellow line) is supplemented by the reverse repo (RRP) offered rate (green) as a subfloor for money market rates. The RRP rate acts as a subfloor because a wider range of counterparties have access to it then to reserve accounts at the Fed (link, full list of RRP counterparties). The market rates for unsecured Fed Funds (white) and Treasury repos (blue) trade between the floor and subfloor. The Fed still provides a ceiling for market rates through the discount window (red), but since the market operates in the elastic region the ceiling does not come into play under normal conditions. To understand where the SRF fits in, we must look back to 2019 when the market rates briefly tested the ceiling.

In early to mid-2018, as show in this chart, market rates traded between the policy floor and subfloor as they do now. At this time, however, the Fed’s balance sheet was shrinking through quantitative tightening, bringing the level of reserves available closer to the minimum needed. By Q2 of 2019, repo and Fed Funds rate had lifted off from the floor, showing that at least some market participants were starting to approach the limits of the elastic region. While it is impossible to set a fixed level of reserves at which money markets transition into the inelastic region (since it varies depending on operational factors and even risk perception), this point was reached in September 2019 when repo rates spiked suddenly to well above the intended ceiling. This was possible because repo dealers (unlike banks), do not have access to the discount window, so the ceiling was not effective in this case. To restore order in the repo market, the Fed began temporary repo operations (which have now been made permanent as the SRF) and added reserves to the system by purchasing Treasury bills.

With the SRF now in place however, it would be difficult for an incident like that of September 2019 to repeat, especially if it is expanded from primary dealers to all FICC member dealers as discussed earlier. While the SRF ceiling will likely not come into play anytime soon (market rates still trade between the floor and subfloor), it could unlock balance sheet efficiencies should the Fed begin another quantitative tightening cycle in the future. By expanding its balance sheet temporarily as needed through the SRF, the central bank could likely somewhat shrink the amount of permanent reserves necessary in the system. By cutting down the tail risk of September 2019 scenarios, the SRF is also relevant to the final topic: the adoption of Term SOFR rates for interdealer trading.

Since the end of the 2008 financial crisis, markets have been well aware that unsecured interbank funding has become mostly a thing of the past and the secured funding transactions that make up SOFR dominate in volume. This shift in market structure has been one of the many driving forces in the effort to move short-term reference rates to a SOFR standard. By recommending Term SOFR rates, the ARRC has proposed a solution to the major hurdle of adapting “spot” overnight SOFR rates to swaps trading, where many contracts depend to some extent on term structure. To solve this issue, CME Group has used SOFR futures prices to calculate an implied term structure. As CME Eurodollar futures, the most traded and liquid interest rate product, are transitioning to CME SOFR futures in mid-2023, the SOFR-linked market is expected to be a very deep and reliable source of data for calculating the implied term structure.

Using these futures prices as the input, CME can calculate an market-implied path of spot SOFR rates over the next few months, using a methodology developed by Fed economists Heitfield and Park (link to the CME whitepaper and link to the original Fed paper). The implied path of spot rates can then be compounded to calculate the implied term rate over a period in the future.

Though a blow-out in spot rates would not necessarily move term rates by the same amount as shown here on the chart of CME Term SOFR rates from their inception at the start of 2019, it would negatively affect financial stability to have a spot rate underlying an increasing volume of derivatives be unexpectedly volatile. In this way the SRF can also bolster confidence in the SOFR transition, by ensuring that the rate upon which all calculations are based remains bounded by a ceiling and a floor.

So what kind of policy environment can we picture if these themes keep developing and changes are implemented successfully? With increased efficiencies in the Treasury repo market introduced by central clearing and the Fed providing temporary balance sheet relief through SRF and RRP operations, we could see a market willing to accept lower levels of permanent Fed balance sheet (reserves). By operating a widely accessible facility, the Fed could also be alerted to developing cash gluts or shortages in the system, and be able to '“fine-tune” its balance sheet size more effectively in future tightening or easing cycles. Finally, with robust policy transmission possible through the FICC-cleared repo market and growing versatility in the derivatives market, we could see SOFR becoming increasingly like a policy rate, slowly edging out the unsecured Federal Funds rate. While all of these are just hypotheticals that are at a minimum a few years off, the events of the last week have moved them closer within the realm of possibility.

In this potential future, we could see market overnight rates again leave the floor regime like they did in early-2019, but now with a robust ceiling allowing markets to move to a hybrid “symmetric corridor” regime. If excess reserves were again trimmed down through quantitative tightening, money markets could operate in the inelastic region as they did before 2008, except now this region would only extend from the RRP floor to the SRF ceiling. It remains to be seen whether things will follow this potential path, but as money markets evolve to seek stability and efficiency and new roads come into view, it may be worth keeping them in mind and tracing where they could lead.

That is all for this Chartbook! Thanks for reading if you made it all the way to the end and hope to see you back soon for another one :)

Cheers,

DC

Hi DC. Any chance you are going to update the blog again. By far the best blog on macro economics I've had the enjoyment of reading. So much appreciated!

Hey DC. With reserve requirements going away per new Fed policy, how does that impact the simple model outlining elasticity for reserves?